Fiscal Analysis of UNLV and UNR Annual Athletics Reports for 2022-2023

[Update: After NFA called out these projected deficits [1], revised Annual Athletics Reports for UNLV and UNR were posted as supplemental materials for the March 1 Board of Regents meeting. UNLV raised various projected revenues to about break even for FY2025 through FY2028. UNR raised projected revenues and reduced some projected expenses, but still projects about $2 million per year in deficits for FY2025 through FY2028 (after spending the $10 million per year in additional institutional support). Neither UNLV nor UNLV provided public explanations for how or why they revised their budget projections.]

Both UNLV and UNR are projecting multi-million dollar annual deficits through fiscal year 2028, which would lead to cumulative deficits of $27 million at UNLV and $38 million at UNR by 2028. At the March 1, 2024, Board of Regents meeting, the Intercollegiate athletics programs at UNLV and UNR will present their 2022–23 budget information for the past five years and projected budgets for the next five years. Institutional presidents and the Board of Regents are responsible for holding athletics programs, as well as other “self-supported” university programs, accountable for fiscally sound practices. Alarmingly, the UNLV and UNR presentations contain no strategies for avoiding these unsustainable budget deficits other than vague mentions of increased gifts or university subsidies.

Here, we provide a fiscal analysis of the two NCAA Division I programs at UNLV and UNR, highlighting issues of concern.

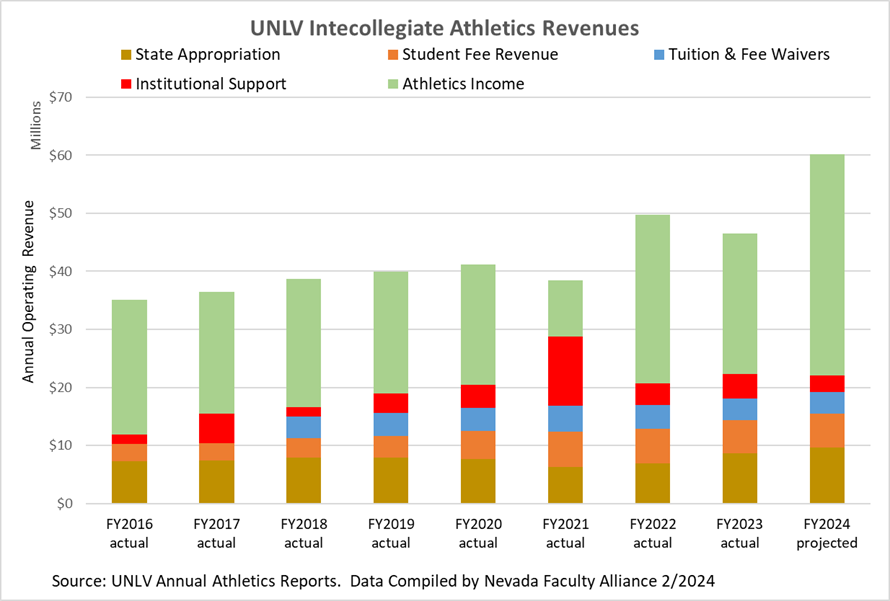

Charts 1A and 1B (below) show the reported* annual operating revenues from the athletics self-supporting budgets for UNLV and UNR, respectively, from FY2016 through FY2023 (actuals) and FY2024 (projected). The revenues are categorized as (a) state appropriations, (b) student fees, (c) tuition and fee waivers, (d) institutional support, or (e) athletics income. Athletics income includes ticket sales, NCAA and conference distribution, media revenue, contributions designated for athletics, and all other program revenue of the athletics programs.

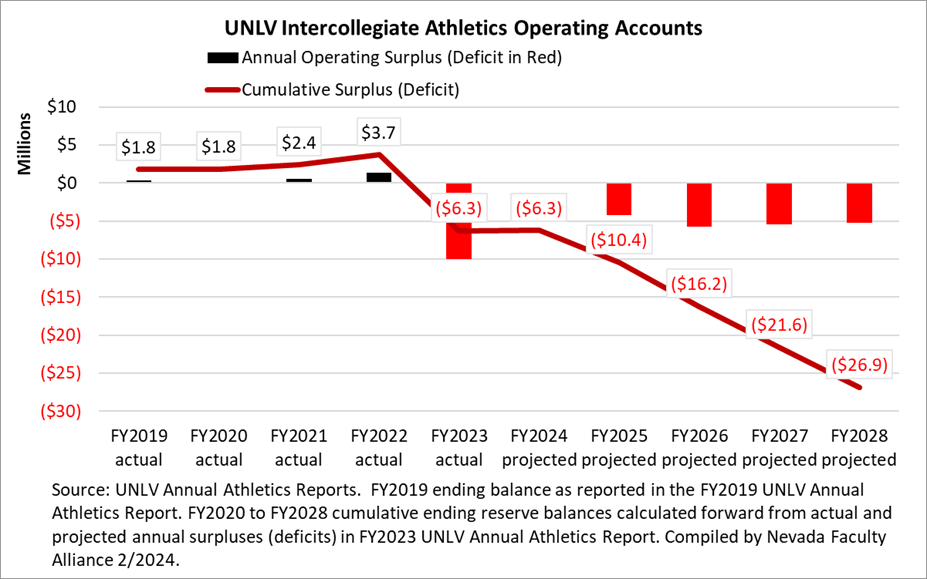

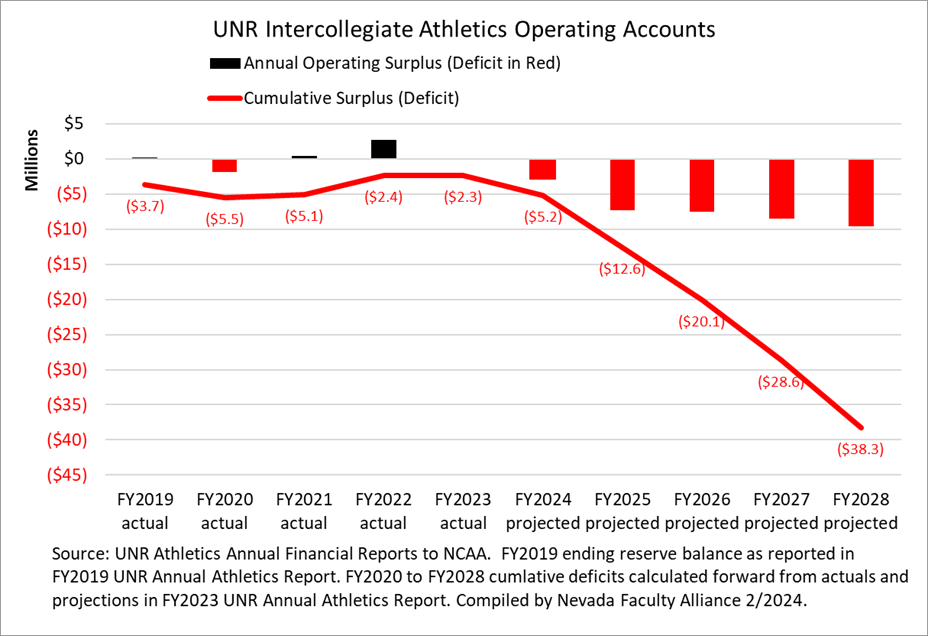

Charts 2A and 2B (below) show the annual operating surplus (or deficits) reported* to NCAA by UNLV and UNR, respectively, along with cumulative surpluses (deficits) starting with FY2019, the most recent annual athletics reports that stated the ending reserve balances, with projections through FY2018. The cumulative deficit for UNR does not include $8.25 million in "historical debt" that was assumed by the university in 2018.

UNLV

UNLV increased institutional support by about $10 million in FY2021 using federal COVID relief funds to cover pandemic-related losses, then returned university support to previous levels (see Chart 1A).

Contributions increased from $4.6 million in FY2023 to a projected $14 million in FY2023, and then are projected to continue at $10 million per year (see “Contributions” under Revenue on page 25 of the UNLV Annual Athletics Report). The source of these higher contributions to the UNLV athletics program was not discussed in the 2023 Annual Athletics Report.

For FY2023, UNLV reported an operating account deficit of $10 million. For FY2024, UNLV projects breaking about even. For FY2025 through FY2028, UNLV is projecting annual deficits of $4.2 to $5.8 million, which would result in a cumulative deficit of $27 million in FY2028 (see Chart 2A). The 2023 UNLV report does not indicate how this deficit will be addressed, only stating the athletics budget office is seeking to clarify institutional support (page 24).

Compensation for coaches at UNLV is increasing from $7.9 million in FY2023 to $11.4 million projected for FY2024, a 44% increase (compared with 12% cost-of-living adjustments).

UNR

UNR increased institutional support by about $10 million per year beginning in FY2021, initially to cover pandemic-related losses (see Chart 1B). UNR projects that higher level of university support to continue through FY2028. Reportedly, the initial funding for the increased institutional subsidy came from federal COVID relief funds while current and future funding is from Marigold Mine royalty income. However, the UNR Marigold Mine royalties are a finite and variable source of funds so it is unclear whether that is sustainable.

For FY2023, UNR reported breaking even with an operating account surplus fo $23,339. For FY2024, UNR projects a deficit of $2.9 million. For FY2025 through FY2028, UNR is projecting annual deficits of $7.4 to $9.7 million, which would result in a cumulative deficit of $38 million in FY2028 (see Chart 2B). These deficits are projected to occur despite the $10 million per year in additional university support. The 2023 report suggests that “additional University support” from UNR will be requested (see “Institutional Revenues” footnote on page 12) in an attempt to maintain parity within the Mountain West conference. That contradicts assurances from the UNR administration that UNR will hold the line on any further increases in institutional support and that Athletics cannot come back and ask for more.

Compensation for coaches at UNR is increasing from $8.8 million in FY2023 to $9.4 million projected for FY2024, a 7% increase (compared with 12% cost-of-living adjustments).

Chart 1A.

Chart 1B.

Chart 2A.

Chart 2B.

###

*Notes: The annual reports for the NCAA Division I programs at UNLV and UNR contain revenue and expense data as reported to the NCAA and as tracked for the self-supporting budgets internally in Workday. The latter exclude various indirect and indirect support, and different accounting standards may apply (e.g., cash vs accrual bases). Also, despite a 2018 NSHE internal audit review designed to make the UNLV and UNR financial reporting more consistent, the format and breakout details of the budget tables in the annual reports are different. Here only apples-to-apples data are compared as we understand the reports. Corrections from authoritative sources are welcome (Contact: kent.ervin@nevadafacultyalliance.org).

References

[1] The revised reports for Agenda item 20 appeared sometime after

5:35 pm on February 27. NFA's

written public comment to Regents reprising the data in this blog post of February 23 was submitted on the morning of February 27 at 7:14 am.